As we look ahead to the year 2024, the mortgage market is poised for a unique set of challenges and opportunities. For Jeff LaBerge, understanding the complex landscape of mortgage rates and housing trends is paramount in the real estate market. In this comprehensive article, Jeff LaBerge will delve into the intricacies of the mortgage market for 2024, offering insights and predictions to help you make informed decisions.

The Continuation of High Mortgage Rates

According to Jeff LaBerge’s research, the outlook for 2024 suggests that mortgage rates will remain “higher for longer”, a point of concern for prospective homebuyers and existing homeowners. In fact, the Fed is expected by some to raise the Fed Funds Rate by an additional 0.25% in 2023. Goldman Sachs, in a recent report, predicted that multi-decade highs in mortgage rates will persist, potentially pushing existing home sales to levels not seen since the early 1990s. The sustained high rates in the vicinity of 8% have deterred current homeowners from entering the housing market, creating a prolonged lack of housing turnover.

The challenge lies in the fact that a significant portion of mortgage borrowers currently hold mortgage with an interest rate well below prevailing mortgage rates. Jeff LaBerge thinks this scenario makes it financially daunting for homeowners to contemplate buying a new home since it would require them to pay-off their existing mortgage and secure a new one at a substantially higher rate, as noted by Goldman Sachs. Jeff LaBerge agrees with Goldman Sachs’ report which expects this scenario to persist, as mortgage rates are unlikely to dip below 7% by the end of 2024.

The combination of high mortgage rates and a low vacancy rate in the housing market creates additional pressure on the construction of new homes. The relationship between housing starts and mortgage rates, which usually holds strong, weakens when homeowner vacancy rates are low, as observed by Goldman Sachs.

Despite the rise in mortgage rates, Jeff LaBerge indicated that housing starts remained resilient in 2022; even rising a few percentage points. However, Goldman Sachs foresees a 4% decline in housing starts in the coming year, with multifamily construction expected to plummet to levels last seen in 2013. This forecast stems from a variety of factors, including homebuilders grappling with an excess of multifamily construction, concerns about a recession, and a decline in new building permits issuance.

The Impact of Supply and Demand

On the demand side, some experts have reported that robust income growth in 2024 is expected to alleviate pressure on multifamily properties, shifting the focus towards higher-income homes, which are typically occupied by owners. This transition is attributed to both economic factors and the changing preferences of homebuyers. Despite this shift, Goldman Sachs predicts that the pace of completions will keep up with the multi-decade high, potentially adding a small increase to the rental vacancy rate.

Renting vs. Buying

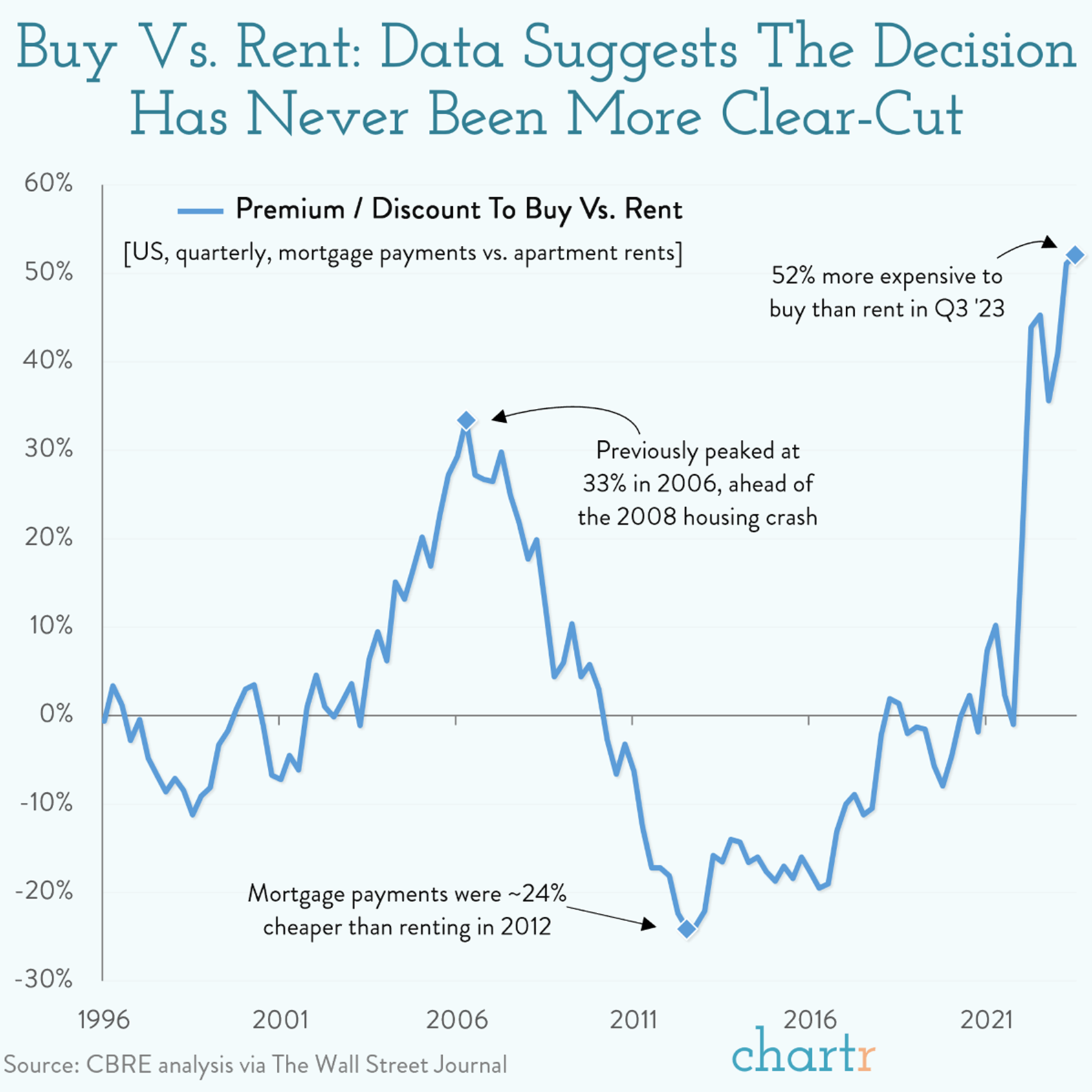

Under this backdrop, the answer to the age old question of whether to “rent vs. buy” has never been more clear. Jeff LaBerge points out that a CBRE analysis, cited by the WSJ finds that it has never made less financial sense to buy home rather than renting one. Per the below chart, mortgage payments are now 52% higher than apartment rents as of September 2023; the highest disparity in decades, if not ever.

Home Price Appreciation and Borrowing Costs

High mortgage rates are anticipated to have a suppressive effect on home price appreciation in 2024. Goldman Sachs predicts a year-over-year increase in home prices of just 1.3%, a significant drop from the estimated 3.4% price increase in 2023. Although current rates are higher, Goldman suggests that prices may trend negatively towards the end of the year [source: Business Insider].

Optimism Amidst Challenges?

Despite the challenges and complexities in the mortgage market for 2024, some experts remain optimistic that rates will come down in 2024.

Jeff LaBerge states that Fannie Mae, a leading source of mortgage financing in the United States, predicts that that 30-year mortgage rates could decline to the 6.7% to 7.1% range in 2024, while the National Association of Realtors anticipates the mortgage rates could be closer to 6% in 2024. The Mortgage Bankers Association forecast predicts that 30-year fixed mortgage rates will go down to 6.1% in Q4 2024 [source: Business Insider].

While industry experts cannot agree precisely how far rates will drop, most of them predict that the 30-year mortgage rate may get back under 7% sometime in 2024.

That being said, Jeff LaBerge believes we are a long way from seeing mortgage rates back down to the 3% range that we have all grown so accustomed to. This would likely require a significant shock to the economy that would cause the Federal Reserve to cut rates back down close to 0%.

Renting vs. Buying

Under this backdrop, the answer to the age old question of whether to “rent vs. buy” has never been more clear. Jeff LaBerge points out that a CBRE analysis, cited by the WSJ finds that it has never made less financial sense to buy home rather than renting one. Per the below chart, mortgage payments are now 52% higher than apartment rents as of September 2023; the highest disparity in decades, if not ever.

This begs the question, what will happen next? Will rents have to increase substantially or will home prices need to tumble down to more reasonable levels?

This begs the question, what will happen next? Will rents have to increase substantially or will home prices need to tumble down to more reasonable levels?

Sources:

Business Insider

Goldman Sachs

CBRE and the Wall Street Journal

{kind=link}